The supply-side impact of planning reforms – land value uplift and construction sector productivity

The Government has committed to reforms to the planning system, which included a significant revision to the National Planning Policy Framework in December 2024. This contained a range of measures, such as significantly higher housing targets for local planning authorities, as well as requirements to review green belt boundaries to meet these new targets.

This article provides more detail underpinning our judgement on the reforms’ supply-side impact, specifically on the higher construction sector productivity we judged the reforms would enable, alongside supporting evidence and the resulting implications for our economy forecast.

Our estimate of the supply-side impact of planning reforms

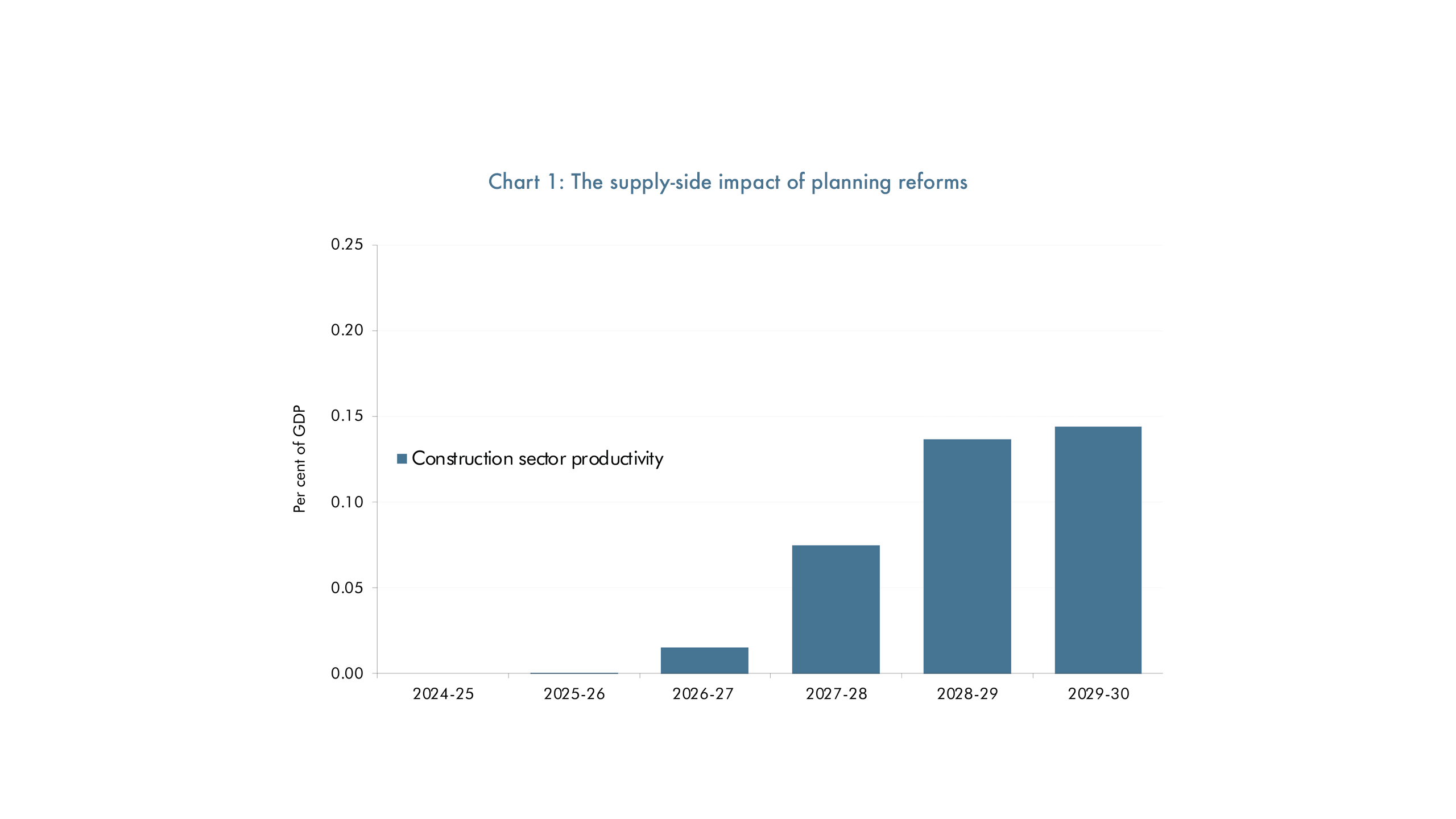

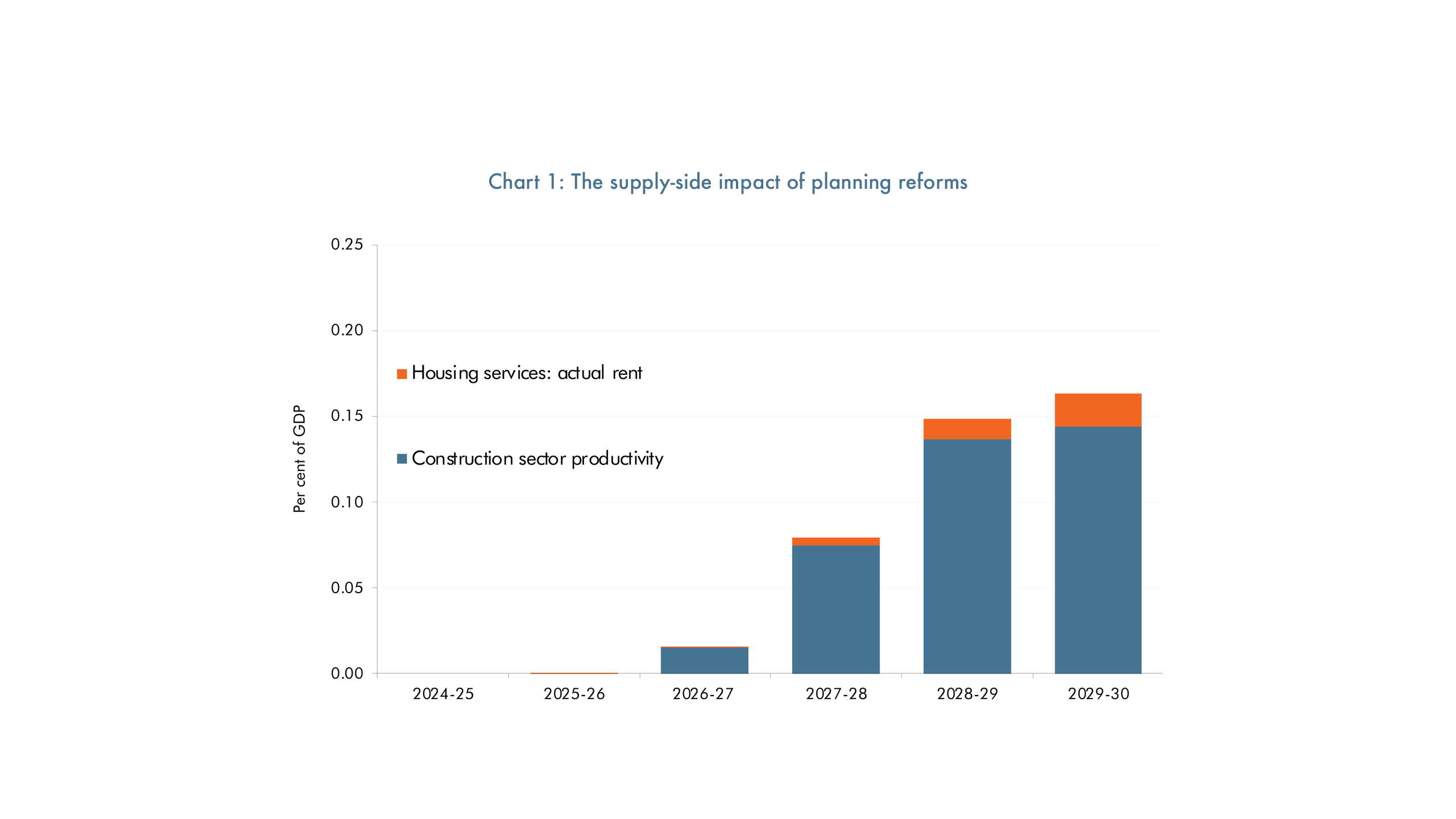

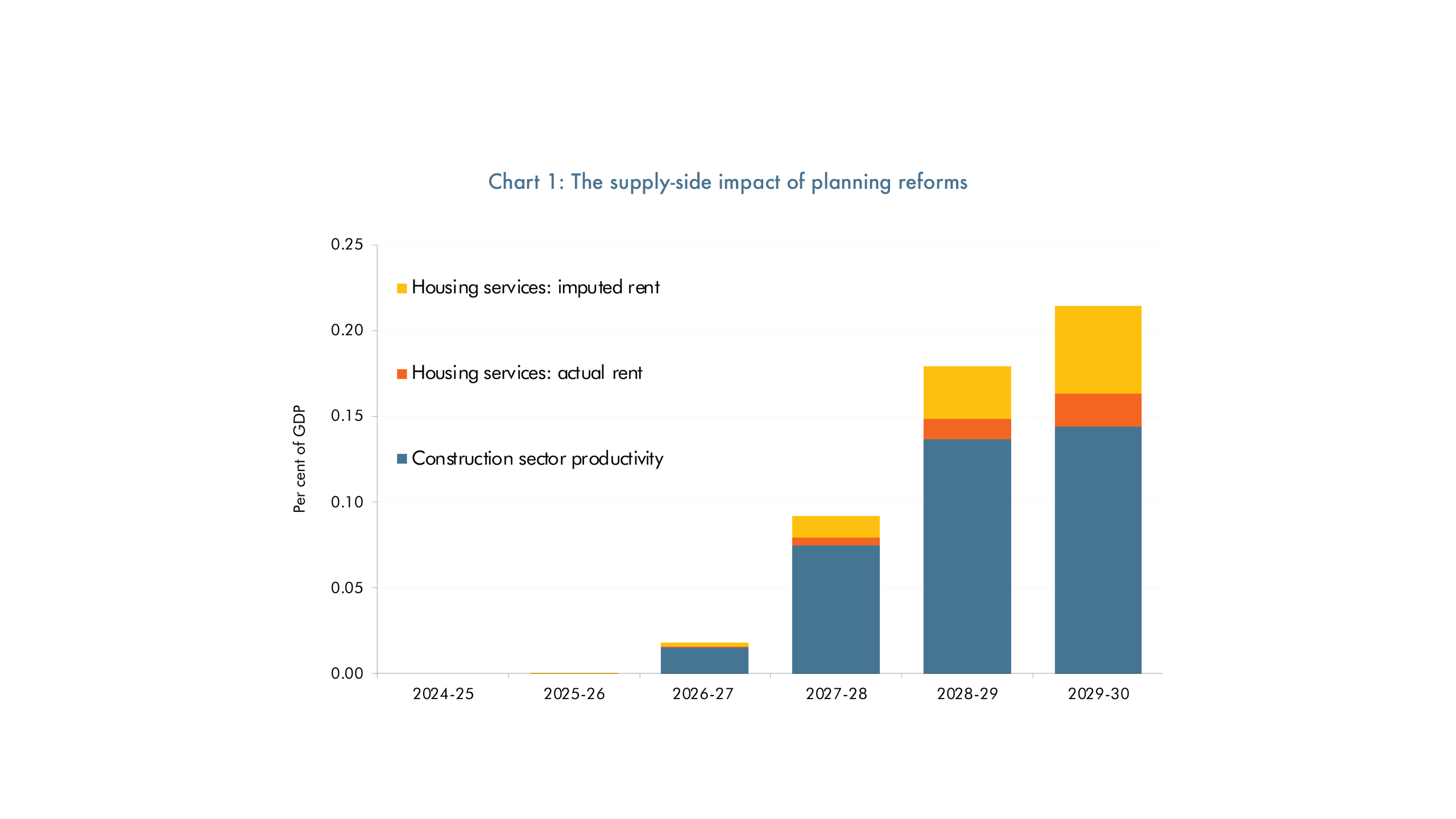

In our March 2025 forecast we estimated that these reforms would lead to a cumulative increase in housebuilding of 170,000 over the forecast period. We judged that this additional housebuilding would result in a 0.2 per cent increase to the level of potential output by 2029-30, two-thirds of which comes from higher construction sector productivity (Chart 1).

How the reforms enable more productive use of land

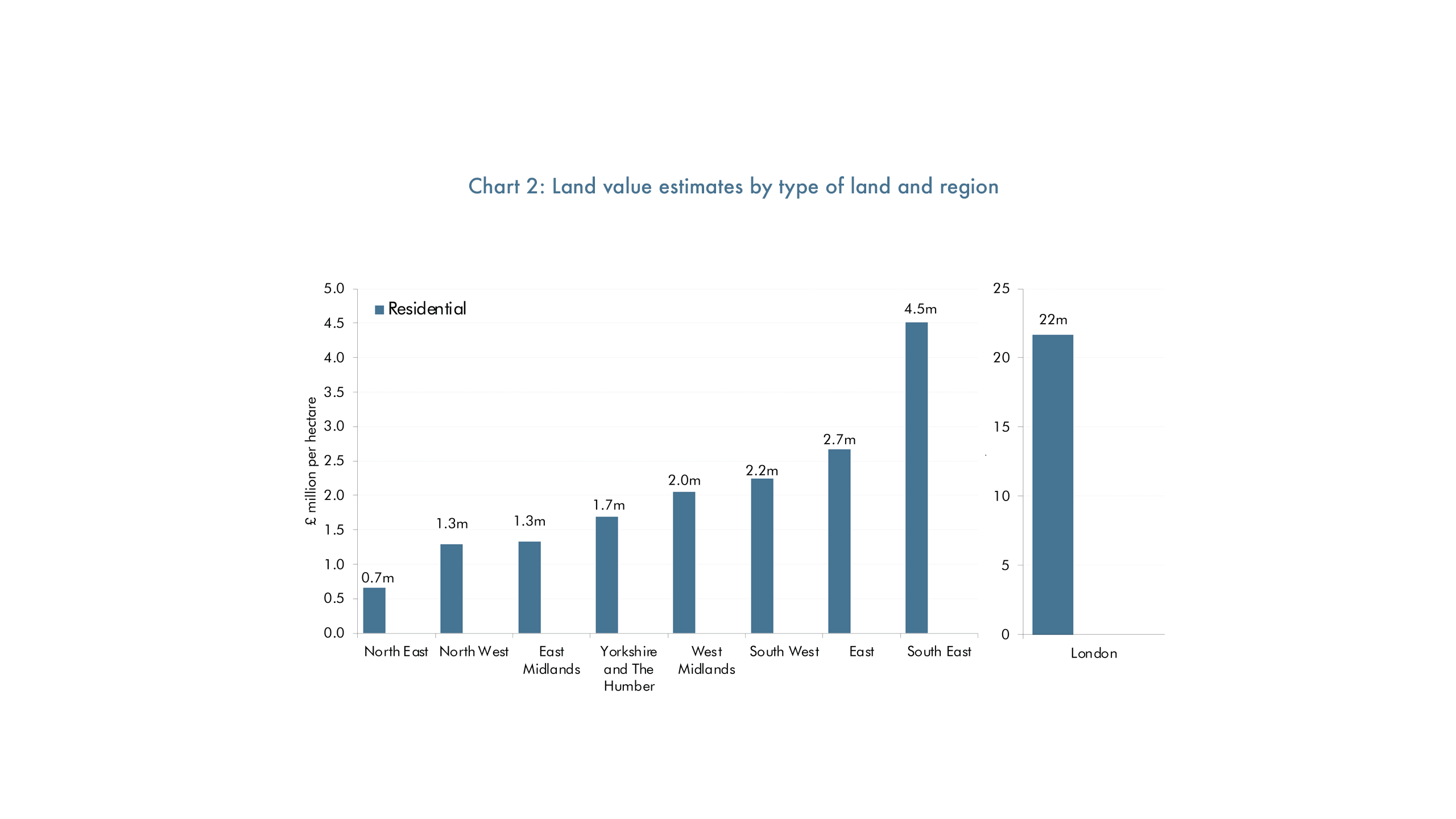

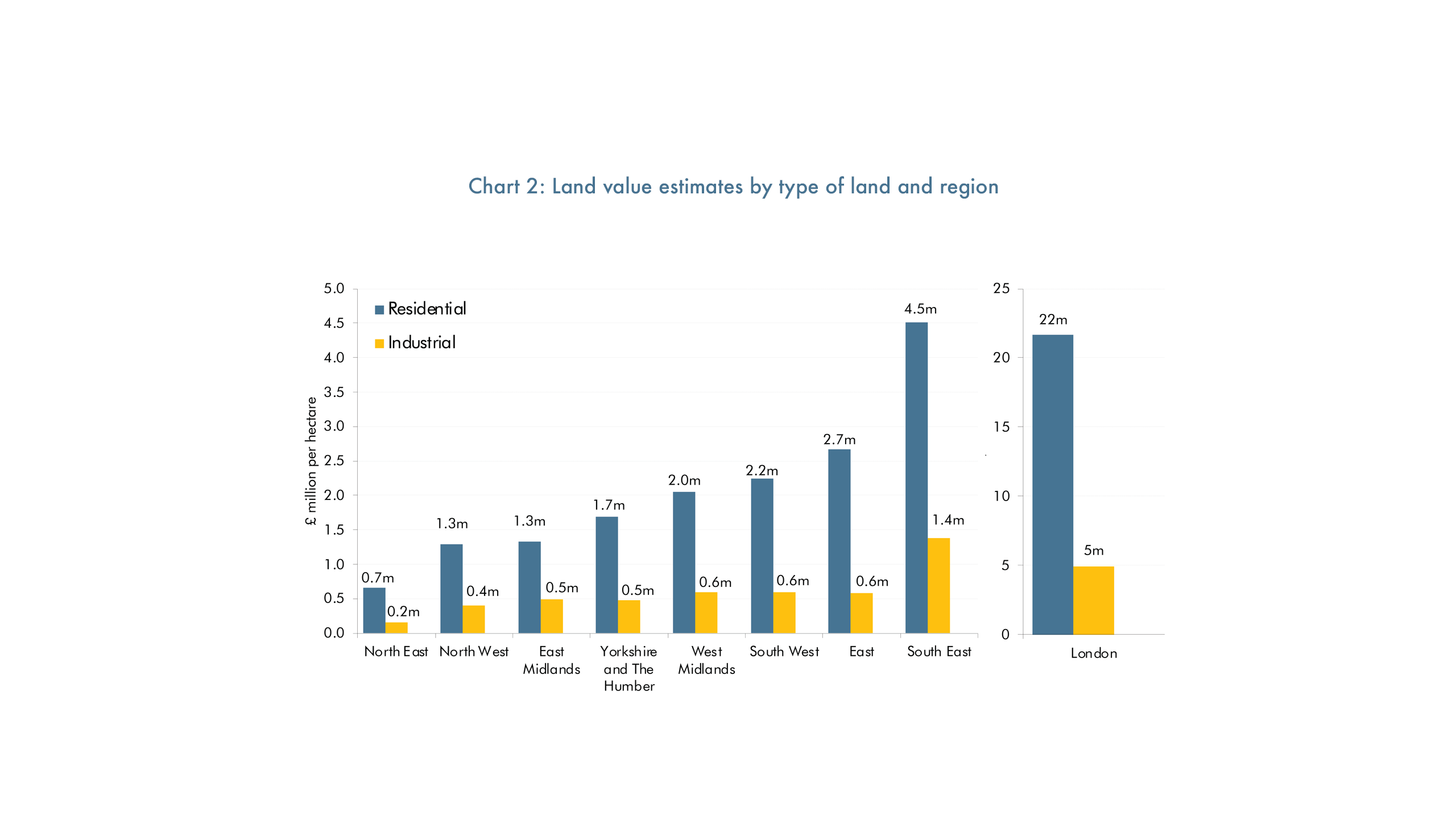

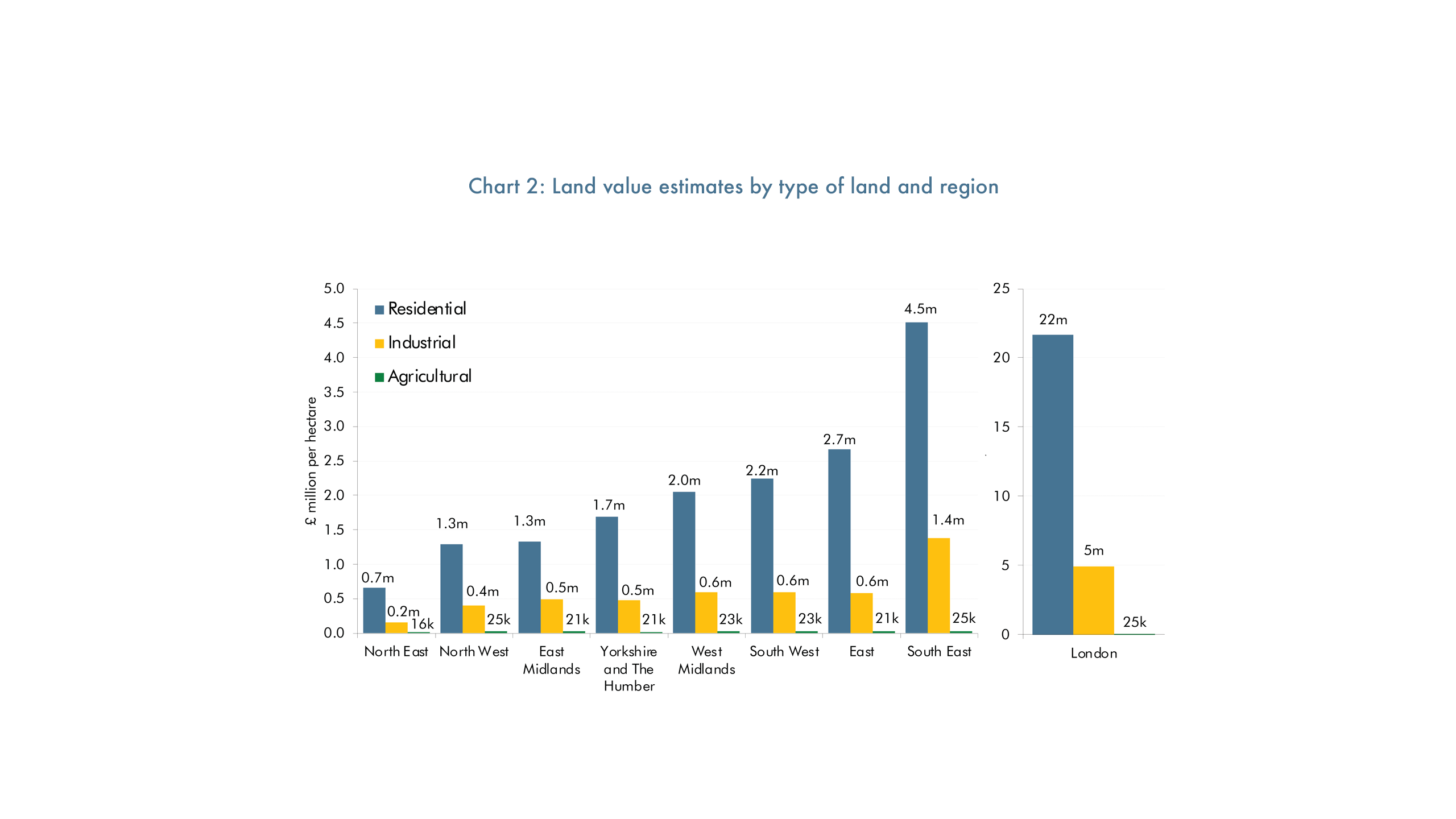

Land is a key input into the production process of all goods and services, with its unit price reflecting the value of the output it is used to produce.1 Land used for residential purposes has a significant premium over land used for alternate purposes according to various datasets – for example, the Valuation Office Agency estimates the per-hectare value of residential land to be £22 million in London, compared to £25,000 for agricultural land (Chart 2). While this premium is largest in London, land for residential use is consistently valued higher than other uses across all the other regions in England.

Green belt land release and planning permission should enable factors of production to be put to more productive use, resulting in uplifts to their values. The reforms will strengthen the presumption in favour of sustainable development which, if triggered, requires local planning authorities to release land for further development unless the adverse impacts of doing so significantly outweigh the benefits. External estimates indicate that up to15 per cent of current green belt land may be re-classified as ‘grey belt’ under these reforms and hence available for development as a result.

Modelling the more productive use of land

The more productive use of land and the resulting higher valuation of it should enable greater activity by the construction sector through, for example, improvements for residential sites.2 In forming our estimate of the supply-side impact from higher construction sector productivity, we made two key judgements on:

- Land’s share of the value of the additional housebuilding. There are large regional variations in land values, as outlined above, as well as in reported measures of land’s share of a house’s value. Figures from major housebuilders report that the purchase price of land makes up around 15 to 20 per cent of the average sales price of new houses sold (although purchase prices will generally not fully account for the increase in value that comes from converting land to more valuable uses). Economy-wide measures of wealth imply over 70 per cent of the total value of the UK housing stock is land. We judged that, of the value from the higher housebuilding enabled by planning reforms, half would be accounted for by land. The skew of regional housing targets towards greater housebuilding in London and the South East, where residential land prices are highest, implies that land is likely to make up a significant share of the value of the additional housebuilding. Though we recognise there is a wide range of uncertainty regarding our 50 per cent judgement.

- The extent to which changes in land values are captured by the construction sector. The uplift in land values reflects the higher potential of residential land relative to its previous use. This land value uplift will be captured by both landowners and developers, with their respective bargaining power determining the share they each get. External estimates point to landowners likely getting the majority of land value uplift, with figures ranging from around half to over three-quarters. We judged that around half of the improvement in land values would reflect construction sector output,3 due to the greater value produced by improvements on the ‘grey belt’ land released by the reforms. Though we again recognise this is a particularly uncertain judgement.

We estimated that higher construction sector productivity would lead to a £4 billion increase in potential output from the 67,000 additional houses in 2029-30 (Table 1). This implies that there is a roughly £60,000 uplift to productivity per house constructed, given the two judgements set out above.4 This increase is largely accounted for by land which previously had a minimal alternative use and will now be used for housing.

Table 1: Economic impact of planning reforms

|

2029-30 increase, £ terms unless otherwise stated |

||

|---|---|---|

|

Per house (£ thousand) |

Total (£ billion) |

|

|

Impact on housebuilding |

||

|

Net additions (thousand houses) |

67 |

|

|

Cumulative net additions (thousand houses) |

170 |

|

|

Impact on economy forecast |

||

|

Residential investment1 |

240 |

16 |

|

Potential output |

90 |

6 |

|

Of which |

||

|

...Housing services2 |

30 |

2 |

|

...Construction sector productivity |

60 |

4 |

|

1We judged that this increased demand would be 'crowded out' in the medium term given little spare capacity in the economy. 2See paragraph 3.40 of our March 2025 Economic and fiscal outlook for more details on the housing services channel. Source: OBR |

||

Feedback

We would welcome any feedback on our modelling, assumptions, or general approach to feedback@obr.uk.

Acknowledgements

We are grateful for the engagement, expertise, and insights from various OBR staff members in compiling this article.

Downloads